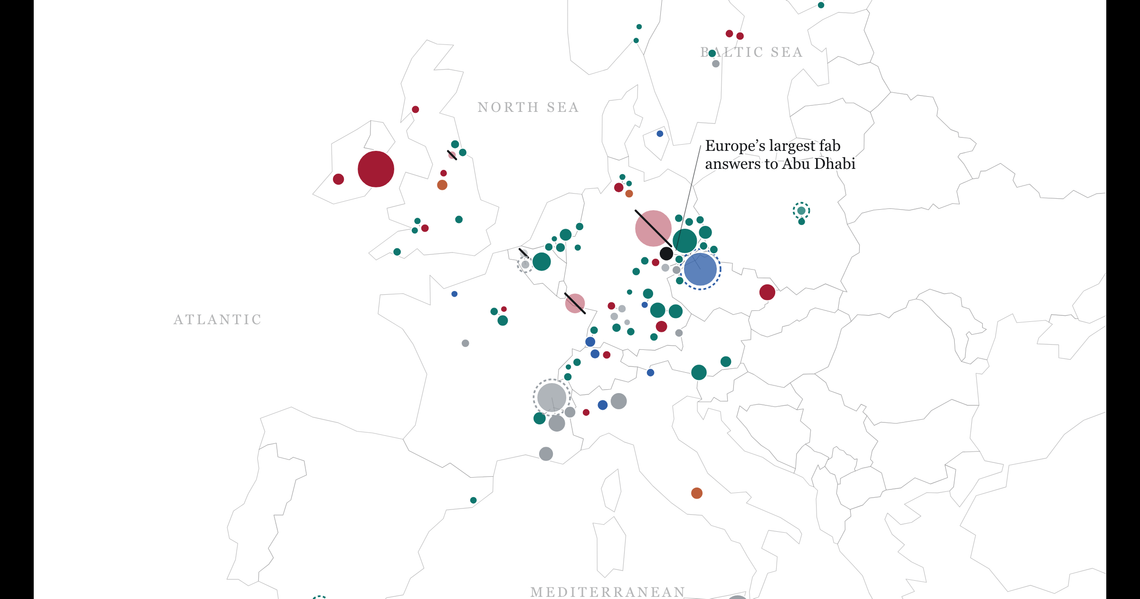

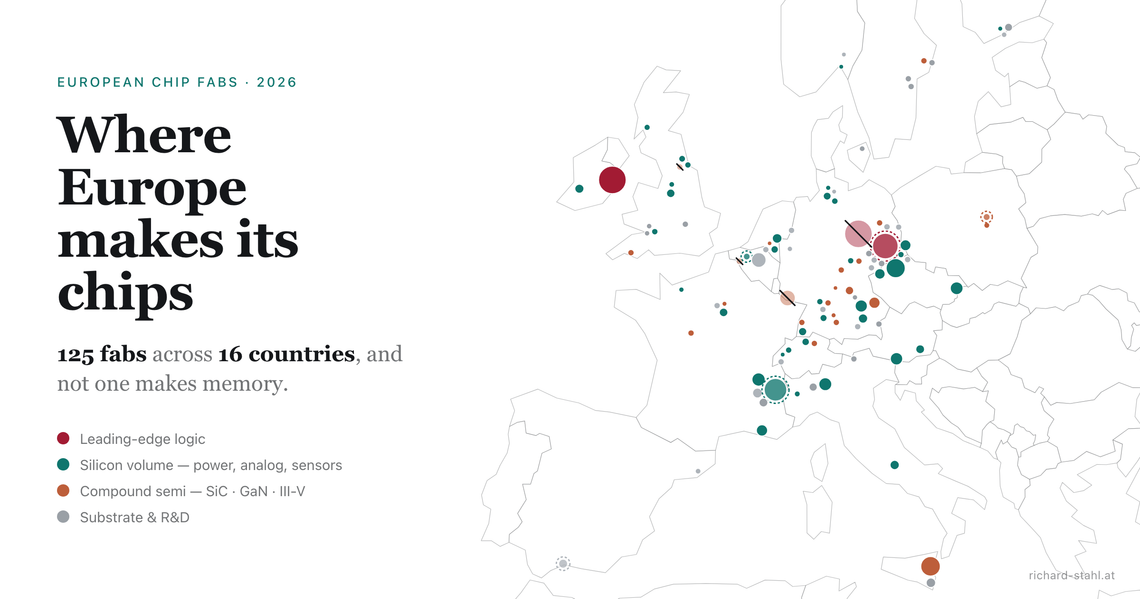

Who Makes Europe's Chips

The five companies that run most of Europe's chip output: Infineon, STMicroelectronics, GlobalFoundries, Bosch and Intel, with revenue and fab data.

The atlas map shows where Europe's capacity is located; these five companies run most of it. Ranked by estimated output from their European fabs, the list is two German groups, one Franco-Italian, and two Americans that have manufactured here for decades. Few chipmakers publish per-fab figures, so the order is an estimate; the concentration is the point. A handful of names carries most of what Europe produces, and each of them would be missed.

1. Infineon — Largest European chipmaker

Munich-based; power semiconductors and automotive chips.

HQ: Neubiberg, Germany · Revenue: €14.66bn (FY2025) On this map: 6 fabs · Villach, Dresden, Regensburg · Est. EU output: not disclosed

Infineon, headquartered just outside Munich, is Europe's largest semiconductor maker by revenue: €14.66 billion in the fiscal year ended September 2025. Half of that came from automotive chips, mostly components that manage power and control functions in cars. The rest comes from power semiconductors for industrial and renewable-energy equipment, sensors, and the security chips inside payment cards and passports. At its last disclosed count the company employed about 58,000 people worldwide.

Its three European manufacturing clusters all sit on this map. Villach in Austria makes power semiconductors, including silicon-carbide and gallium-nitride devices for electric vehicles, on 200mm and 300mm wafers. Dresden runs power, sensor and microcontroller lines and is adding a €5 billion 300mm Smart Power Fab, now under construction. Regensburg makes power and sensor chips on older equipment. A prolonged outage at any of the three would reach European carmakers and power-equipment manufacturers within weeks.

Automotive chips were 50% of Infineon's €14.66bn FY2025 revenue, its largest single business.

2. STMicroelectronics — Most fabs on the map

Franco-Italian; microcontrollers, sensors and silicon-carbide power.

HQ: Geneva, Switzerland · Revenue: $11.8bn (2025) On this map: 11 fabs · France, Italy, Sweden · Est. EU output: Crolles financed for 360k wafers/yr

STMicroelectronics is the Franco-Italian chipmaker, listed in Paris and Milan, with $11.8 billion of revenue in 2025 and about 50,500 employees. The French and Italian states jointly hold 27.5% of it through a holding company. Its products are unglamorous and everywhere: STM32 microcontrollers run appliances and car electronics, its motion sensors sit inside phones, and its power chips, increasingly silicon carbide, manage energy in electric vehicles and industrial equipment.

ST operates eleven of the map's fabs across France, Italy and Sweden. Crolles makes 300mm logic wafers on FD-SOI, a low-power process, and is financed to reach 360,000 wafer starts a year. Rousset makes microcontrollers and secure chips, Tours power diodes and gallium-nitride devices. In Italy, Agrate Brianza produces smart-power chips and Catania is building a €5 billion silicon-carbide campus, fed by ST's own substrate plants in Catania and Norrköping. Without ST, Europe's carmakers would lose their largest domestic source of the chips that run motors, chargers and control units.

The French and Italian states jointly hold 27.5% of ST; Crolles is EIB-financed to reach 360,000 300mm wafer starts a year.

3. GlobalFoundries — Largest single site

US-listed foundry; Dresden Fab 1 is Europe's biggest chip factory.

HQ: Malta, NY, USA · Revenue: $7.4bn (2023) On this map: 1 fab · Dresden (Fab 1) · Est. EU output: 950k wafers/yr (300mm-eq)

GlobalFoundries manufactures chips that other companies design, the business model known as a foundry. Spun out of AMD in 2009, majority-owned by Abu Dhabi's Mubadala fund and listed in New York since 2021, it took in $7.4 billion in 2023 and sits among the largest foundries behind TSMC. It deliberately skips the smallest transistor geometries and concentrates on specialty processes for cars, radios and low-power devices.

Fab 1 in Dresden is Europe's largest single chip factory: 950,000 300mm-equivalent wafers a year by the company's own rating, made on a 22-nanometre low-power process (FD-SOI) for cars, industrial sensors and phone radios. GlobalFoundries has committed a further €1.1 billion to push past one million wafers a year by 2028, and in December 2025 the Commission cleared €495 million of German state aid toward the expansion (case SA.118843). Dresden is also most of Europe's open contract capacity: without it, a European chip designer would have almost nowhere on the continent to get volume silicon made.

Fab 1 runs about 950,000 300mm-equivalent wafers a year, more than any other single fab site in Europe (GF, 2025).

4. Bosch — The carmaker's own fabs

World's largest car-parts group; makes its own sensors and power chips.

HQ: Gerlingen, Germany · Revenue: €90.3bn group (2024) On this map: 2 fabs · Reutlingen, Dresden · Est. EU output: not disclosed

Bosch, the world's largest automotive supplier, also makes its own chips: the MEMS sensors that let cars and phones sense motion and pressure, application-specific chips for engine and safety systems, and silicon-carbide power devices for EV inverters. It is the only car-parts group that both designs vehicle systems and fabricates the chips inside them. Group revenue was €90.3 billion in 2024; semiconductor sales are not broken out.

Both fabs are German. Reutlingen, in production since the 1970s on 150mm and 200mm wafers with about 8,000 staff, makes automotive chips, MEMS sensors and silicon-carbide devices, and is being expanded with roughly €250 million of new investment. The €1 billion Dresden 300mm fab, opened in 2021, makes automotive and power chips, with MEMS lines to follow in 2026. Europe's car industry builds safety and powertrain systems around parts from these two sites.

Bosch says more than half of all new smartphones worldwide contain one of its MEMS sensors.

5. Intel — The only leading edge

US processor maker; runs Europe's only leading-edge volume fab.

HQ: Santa Clara, CA, USA · Revenue: $52.9bn (2025) On this map: Leixlip Fabs 34 & 24 · Magdeburg cancelled · Est. EU output: not disclosed

Intel is the world's largest maker of x86 processors, the chips at the heart of most PCs and servers. Revenue was $52.9 billion in 2025, flat on 2024 after several years of decline; its foundry unit lost about $13 billion in 2024, and the company cut roughly 15% of its workforce. It trails TSMC in manufacturing and Nvidia in AI chips.

Intel has manufactured at Leixlip, outside Dublin, since 1989. Fab 34, opened in 2023 at a cost of about €17 billion, prints chips with extreme-ultraviolet (EUV) light on the Intel 3 process, the only line in Europe making leading-edge logic at volume; the older Fab 24 next door still runs 14nm. Together they employ about 5,000 people. The €30 billion fab Intel announced for Magdeburg in 2022 was cancelled, the dark slash on this map. Without Leixlip, European output of leading-edge processors would be zero.

Fab 34 is Europe's first and only high-volume EUV fab; it doubled Intel's Irish capacity when it opened in 2023.

Ranking is an editorial estimate of front-end wafer output at European sites; chipmakers rarely publish per-fab output figures. Close behind the five: ams OSRAM (Premstaetten, Regensburg), NXP (Nijmegen, plus the ESMC venture in Dresden with TSMC, Bosch and Infineon), X-FAB (Erfurt, Dresden, Itzehoe, Corbeil-Essonnes), Nexperia (Hamburg, Manchester) and onsemi (Rožnov). Company figures as of early 2026, from the sources linked per profile; every dot on the map carries its own fab-level sources.

Part of the European Semiconductor Atlas — open, source-verified data on Europe's chip supply chain. The interactive map lives here.

Thinking out loud, by email

Occasional notes on technology, Europe, and whatever else has my attention. No spam — unsubscribe anytime.

{kind=link}

Member discussion